Awesome service John went out of his way to help make this deal happen. There are not many people with the integrity, as focused, and dedicated in this business as John. I am looking forward to working again with John and his team! Great experience!

When Money Is Tight, You Need Solutions—Not More Stress.

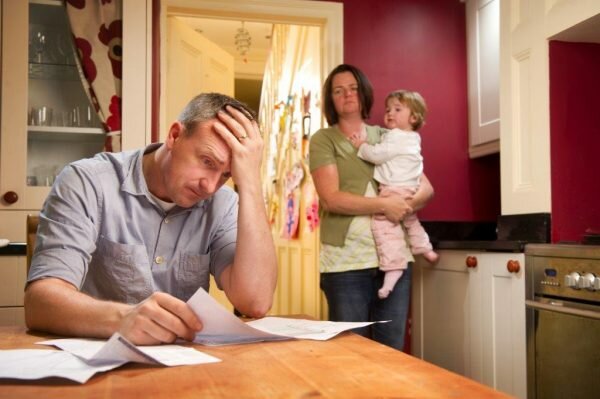

Financial hardship can happen to anyone.

Whether you’re behind on mortgage payments, facing foreclosure, dealing with unexpected medical bills, carrying overwhelming debt, or simply can’t afford your home anymore, you don’t have to face it alone.

At Cash Home Buyer Florida, we help homeowners across Florida sell quickly with a fair, transparent cash offer—so they can move forward with confidence.

In life, situations arise that you just don’t plan on. These situations can affect your ability to pay your mortgage on a timely basis – loss of employment, sickness, excessive debts, incarceration, mounting bills, etc. Lenders are not concerned why you’re unable to pay your mortgage – they just want their money and they’ll foreclose on your home to recover the money they’re owed. Obviously, this is not what you want and the idea of going into foreclosure can be scary, stressful, leaving you on an uncertain path to find solutions to stop your foreclosure – and sleepless nights. Below are some ideas to consider on how to stop your foreclosure in Florida.

Don’t avoid the problem. The first time you miss a mortgage payment you know there’s a problem. Don’t fall into the trap of denial and avoidance. Get proactive. Don’t wait for things to get worse before you start looking for solutions; make the decision now and avoid losing your home. Many options exist to stop foreclosure in Florida and you need to know your options and the choice that makes the most sense in your situation. Let’s find a solution now.

We Make Selling Simple

Complete the form below or Call or Text Us! (386) 383-2085

✓

Sell Your Home As-Is

✓

No Repairs or Cleaning

✓

No Realtor Commissions

✓

No Closing Costs

✓

Fair, Transparent Cash Offers

✓

Close on Your Timeline

Real Estate Investors prefer buying houses before the foreclosure process is complete. Why? Once the foreclosure is completed, you’ve lost the house for good. When selling your house to a real estate investor, you can sell your house fast and you just might walk out of your situation with some profit. Even selling your house for little or no profit is better than losing the house completely to the bank and further affecting your future ability to obtain credit. Real estate investors deal in distressed properties and distressed situations all the time, so they can provide you with tips and offer realistic solutions on how to stop home foreclosure.

There are many specialized real estate professionals in Florida that are not necessarily Realtors. Real Estate Investors are specialized. Realtors are basically looking to make a commission on the sale of your home, and they are trained to market your house for the most profit. Their services are useful when the seller is not in distress. Unfortunately, you’re in distress and you don’t have the luxury of time…the clock is ticking, and you need a solution now from someone who does this on a daily or weekly basis. Most Realtors are unaware of the strategies we employ to help you. That’s why you need a real estate investor

Financial challenges can be overwhelming.

Choosing the right company to help shouldn’t be.

For more than a decade, Cash Home Buyer Florida has helped homeowners throughout Florida navigate difficult financial situations with honesty, transparency, and respect.

✔ Florida-Based Local Experts

✔ 10+ Years Helping Homeowners

✔ Transparent, No-Pressure Offers

✔ Better Communication

✔ Personalized Service

✔ No Hidden Fees

Our goal isn’t simply to buy houses.

It’s to help people regain financial peace of mind.

| Traditional Home Sale | Cash Home Buyer Florida |

|---|

| Repairs Required | ✔ None |

| Realtor Commissions | ✔ None |

| Cleaning & Staging | ✔ None |

| Financing Delays | ✔ None |

| Multiple Showings | ✔ None |

| Months to Sell | ✔ Often Much Faster |

Our focus is simple:

Helping Florida homeowners move forward with honesty, transparency, and respect.

Life is unpredictable, and financial struggles can arise when you least expect them. Whether you’re facing foreclosure, overwhelming debt, job loss, divorce, or unexpected medical bills, selling your house for cash can provide a fast and stress-free solution to regain financial stability.

At Cash Home Buyer Florida, we specialize in helping homeowners like you sell quickly for a fair cash offer, so you can move forward without the burden of a house that’s weighing you down.

Please complete the form here or give us a call at (386) 383-2085 to discuss the sale of your home.

Many homeowners in this situation still have options. Contact us as early as possible so we can discuss your circumstances.

Many of the homes we purchase are below market value (we do this so we can resell at a profit to another home owner). We are looking to get a fair discount on a property. However, in our experience, many sellers aren’t necessarily expecting a large “windfall” on the property but rather appreciate that we can offer cash, we close very quickly (no waiting for financing), and no time or effort, or expense is required on your part of fix up the property or pay agent fees. If that’s what you’re looking for and you see the value in getting your home sold fast…let’s see if we can come to a fair win-win price. (Besides, our no-obligation pricing commitment means that you do not have to move forward with the offer we give… but it’s good to know what we’re offering!)

Great question, and we’re an open book: Our process is very straightforward. We look at the location of the property, what repairs are needed, the current condition of the property, and the value of comparable homes sold in the area recently. As you know, home values have taken a huge hit in the last 5 years and most areas still haven’t seen prices come back up. We take many pieces of information into consideration… and come up with a fair price that works for us and works for you too.

This is what makes us stand out from the traditional method of selling your home: There are NO fees or commissions when you sell your home to us. We’ll make you an offer, and if it’s a fit then we’ll buy your home (and we’ll often pay for the closing costs too!). No hassle. No fees. We make our money after we pay for repairs on the home (if any) and sell it for a profit (we’re taking all of the risks here on whether we can sell it for a profit or not, once we buy the home from you… the responsibility is ours and you walk away without the burden of the property and its payments… and often with cash in your hand).

Real estate agents list properties and hope that someone will buy them. The agent shows the properties to prospective buyers if there are any (the average time to sell a property in many markets right now is 6-12 months) and then takes a percentage of the sale price if they find a buyer. Oftentimes, the agent’s commission is 3-6% of the sale price of your home (so if it’s a $100,000 home, you’ll pay between $3,000 – $6,000 in commissions to an agent). Agents provide a great service for those that can wait 6-12 months to sell and who don’t mind giving up some of that sale price to pay for the commissions. But that’s where we’re different: We’re not agents, we’re home buyers. Our company actually buys homes. We don’t list homes. Since we’re actually the ones buying the home from you, and we pay with all cash…we can make a decision to buy your home within a couple of days (sometimes the same day). Again, we make our living by taking the risk to buy the home with our own cash, repair the home, and market it ourselves to find a buyer (which is the hard part in this market).

There is absolutely zero obligation for you. Once you tell us a bit about your property, we’ll take a look at things, maybe set up a call with you to find out a bit more, and make you an all-cash offer that’s fair for you and fair for us. From there, it’s 100% your decision on whether or not you’d like to sell your home to us… and we won’t hassle you, won’t harass you… it’s 100% your decision and we’ll let you decide what’s right for you.

Check out what our clients have to say about us!

Awesome service John went out of his way to help make this deal happen. There are not many people with the integrity, as focused, and dedicated in this business as John. I am looking forward to working again with John and his team! Great experience!

I worked with John Patton in the sale of my property. There were a few complications along the way which John greatly attributed his time to getting resolved in a timely manner. John really fought for me in the sale of my property and I couldn’t be more pleased with him and the service that he provided. I am thankful for his diligence in helping me. I would highly recommend him.

John was amazing start to finish. He took what was honestly a nightmare for our family and turned it around. He was easy to work with and straightforward, there were no games or low offers, and the whole thing was kind of a relief. I don’t think I’ve ever been happier to have called a random number on the internet just to see what they say, he saved us countless hours of work and money just to sell anyway.

John was straight-forwarded, courteous, and sincere from the start. Communications / responses were swift. The entire process was uncomplicated and smooth. I highly recommend them.

I can’t recommend John Patton with Cash Home Buyer Florida enough! From start to finish, the process was smooth, transparent, and incredibly fast. I needed to sell my home quickly due to a job relocation, and he ensured my timeline was met. He was extremely professional, communicative, and made me feel confident every step of the way. If you’re looking to sell your home without the stress of traditional real estate, this is the company to go with. Thank you for making this such a positive experience!

What a great experience from the start…I was helping my grandma (granny) sell her home that got flooded during the last hurricane…she’s 80 years old and didn’t want to deal with rebuilding her home…I called Cash Home Buyer and felt a breath of fresh air with their professionalism, help through the process, and how quickly and efficient the process was…I would recommend them if anyone is looking to sell their home at a cash price!!! Thanks and God bless!!!